On March 12, 2026, Bill C-4, the federal legislation Making Life More Affordable for Canadians Act (the “Act”), received Royal Assent. The measure forms part of the federal government’s housing affordability initiatives and is designed to reduce the upfront cost of purchasing a newly constructed home in Canada.

The Act includes a number of tax measures, most importantly, it eliminates “the Goods and Services Tax (GST) for first-time home buyers (FTHBs) on new homes up to $1 million and reducing the GST for first-time home buyers on new homes between $1 million and $1.5 million.”

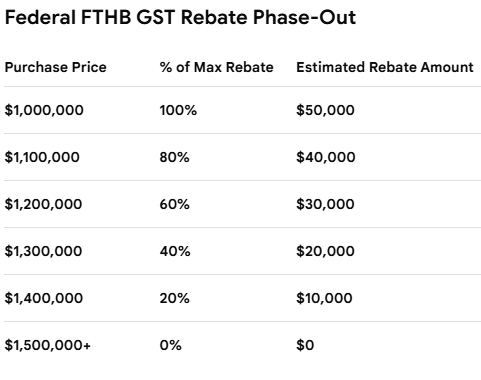

Key Features: The new FTHBs’ GST Rebate applies to the purchase of qualifying newly constructed homes and provides the following benefits:

- At or below the purchase price of $1 million, the rebate is 100% (5% GST) (up to a maximum rebate of $50,000 at a purchase price of $1,000,000);

- Between $1 million and $1.5 million, the maximum rebate is gradually reduced on a sliding scale (i.e. For every $100,000 you go above $1 million, you lose 20% of the maximum rebate (or $10,000));

- At or above $1.5 million, there is no rebate on any part of the purchase price.

Under this new law, as a first-time home buyer, you may be eligible for the FTHB GST/HST rebate in addition to the existing GST/HST new housing rebate, which can apply to any home buyer, not just FTHBs. Where both rebates apply, the FTHB GST/HST rebate acts as a top-up to the existing GST/HST new housing rebate.

This measure significantly expands relief compared to existing GST new housing rebate rules and is intended to improve affordability for individuals entering the housing market for the first time.

Eligibility: To qualify for the rebate, the purchaser must meet specific personal and property-related conditions:

- Personal Qualifications: To be considered a First-Time Home Buyer (FTHB), an individual must:

- Be at least 18 years of age.

- Be a Canadian citizen or permanent resident.

- The “Four-Year” Rule: You must not have inhabited a home owned (wholly or jointly) by yourself or your spouse/common-law partner as a primary residence within the current calendar year or the previous four calendar years. Note the difference from the British Columbia Property Transfer Tax for FTHB, which is applicable once during your lifetime anywhere in the world.

- Rebate Exclusivity: Neither you nor your spouse/common-law partner can have previously received an FTHB GST/HST rebate, ever.

- “At Least One” Rule: To qualify for the rebate, only one person in the purchasing group needs to be a first-time home buyer.

- Property Requirements: The rebate applies exclusively to newly constructed or “substantially renovated” residential properties intended for use as the purchaser’s primary place of residence. This includes:

- Traditional detached homes and semi-detached builds;

- Homes on leased land (with a lease term of at least 20 years or a purchase option);

- Mobile, modular, or floating homes; and

- Shares in a co-operative housing corporation.

“Substantially Renovated” means the following:

- The 90% Rule (“All or Substantially All”): While not strictly defined in law, the CRA typically interprets this as at least 90% of the building’s interior being removed or replaced. This is measured by comparing the renovated square footage or room count against the total original structure.

- Excluded Elements: When calculating the 90% threshold, you do not include the foundation, external walls, interior load-bearing walls, floors, roof, or staircases. However, if these structural elements are also replaced, they can support the “new build” classification.

- Total Overhaul: As reinforced by case law (Whittal v. Her Majesty The Queen), the renovation must be a “near-total” transformation of the existing building to qualify for tax purposes.

- Major Additions: Simply adding a room isn’t enough. For an addition to count toward a “substantial renovation,” it must significantly increase the building’s size and functionality, effectively turning the old structure into a minor component of a new residential entity.

Critical Timing & Effective Dates

The rebate generally applies to Agreements of Purchase & Sale entered into on or after March 20, 2025, and before 2031.

Important Legal Note for Investors and Entities & Real Estate Professionals/Advisors

It is critical to note that corporations and partnerships are ineligible for the New FTHB GST Housing Rebate. To ensure eligibility, the property must be purchased in the names of individuals.

Given the recent implementation of this legislation, the CRA is expected to release updated forms and further administrative requirements shortly. We recommend consulting with legal counsel to ensure your purchase agreement and application timing align with these evolving regulations and acts.

How can we help

Our firm is monitoring developments related to the new rebate and forthcoming CRA guidance. If you are considering purchasing a newly constructed home or would like assistance determining whether you may qualify for the rebate, please contact me for further information at somal@pushormitchell.com.

Disclaimer: The content made available on this website has been provided solely for general informational purposes as of the date published and should NOT be treated as or relied upon as legal advice. It is not to be construed as a representation, warranty, or guarantee, and may not be accurate, current, complete, or fit for a particular purpose or circumstance. If you are seeking legal advice, a professional at Pushor Mitchell LLP would be pleased to assist you in resolving your legal concerns in the context of your particular circumstances.

It is prohibited to reproduce, modify, republish, or in any way use content from this website without express written permission from the Chief Operating Officer or the Managing Partner at Pushor Mitchell LLP. Third-party content that references this publication is not endorsed by Pushor Mitchell LLP and in no way represents the views of the firm. We do not guarantee the accuracy of, nor accept responsibility for, the content of any source that may link, quote, or reference this publication.

Please read and understand our full Website Terms of Use and Disclaimer here.